A fundamental paradox lies at the heart of the clean energy transition. Batteries, which are vital in our battle to decarbonise, are themselves responsible for substantial environmental harm. The materials they require and the dirty energy used to fuel their production pose a dilemma: at what point does clean energy actually become clean?

Fortunately, Norwegian firm Freyr may well have the answer.

The Curation Collective was recently joined by Jeffrey Spittel, VP of Investor Relations at the firm, to discuss Freyr’s crucial role in cleaning up the energy transition’s dirtiest industry.

Utilising the abundant renewable energy resources (accounting for 98% of electricity generation) available in Norway, they are developing a lithium-ion battery that is truly green.

And when they say green, they mean it. Freyr aims to:

Produce and sell batteries that over their lifetime may abate 345 mt of CO2 – equivalent to the annual emissions of 130 million combustion engine cars.

Deliver battery cells with ~zero CO2 emissions from the cell manufacturing process.

Maintain a supply chain that delivers a CO2 footprint of 15 kg CO2 per KWh battery capacity produced – significantly less than today’s global average of around 80-100 kg CO2 per KWH.

Next week, we will be digging deeper into Freyr’s mission and its future ambitions to decarbonise global transportation and energy systems…

Toyota & CATL eye mass-production of solid-state batteries

CATL and Toyota are the two companies making the most noise about solid-state batteries with CATL announcing it will move into production as early as Q1 2024, while Toyota touts 2027 as its target for mass production.

Toyota claims its batteries will have a range of 1,200km and charge in 10 minutes or less – if there was one technological breakthrough that could turn the entire auto industry on its head, this is it.

A long way to go but well worth monitoring.

Over-optimistic Tesla

Remember Dieselgate? I wonder if we could be on the verge of a similar scandal involving misleading in-vehicle software emerging…

Tesla is facing an investigation from the US Department of Justice over the estimated driving range of its electric vehicles. The suit allegedly refers to some overly optimistic range figures displayed in Tesla’s software – not ideal if you’re trying to get to a charger on time…

Every media or information medium undergoes a revolution that irrevocably transforms how it is consumed.

Whether it’s Spotify’s effect on music streaming, Netflix’s on film and television consumption or – if we want to go way back – the invention of the printing press on the written word, technological advancements or new modes of thinking transform how society creates, distributes, and consumes information.

It may sound hyperbolic, but the next paradigm shift in information consumption may well be in the world of financial data and analytics following the London Stock Exchange Group’s (LSEG) partnership with tech giant Microsoft.

It promises a seismic shakeup to the financial information landscape, perhaps even consigning financial terminals (a computer system that enables users to access real-time market data) to the annals of history in the same way Netflix did to Blockbuster, Spotify did to iTunes and CDs, and the printing press did to handwriting.

To guide us through this transition, the Curation Collective welcomed the Director of Investor Relations at LSEG, Peregrine Riviere, to the club in September.

Not just a stock exchange

If you’re confused about why a stock exchange operator is partnering with a software company, you’re probably not alone. The LSEG is one of the most misunderstood companies on the market; given its name, most expect managing London’s stock exchange to be the group’s primary focus, but this side of the business accounts for just 3% of group turnover.

Instead, the company’s primary focus is Generative AI, LLMs, financial data and analytics, and now, attention has shifted to infiltrating Microsoft Office’s global user base. Operationally, LSEG is a subscription business with 73% recurring revenue, and a massive 70% of business comes from its data and analytics offering, with its LSEG Workspace platform and Eikon terminals making up a significant chunk of revenues.

Once LSEG’s financial data and LLMs are embedded in the Microsoft suite, Teams could become the new secure chat and Office the new terminal. It’s a timely development as “traditional” financial terminals are becoming increasingly incompatible with 21st-century workflows, just as going to a store and renting a DVD became an outmoded form of film consumption in our digitalised era.

To contextualise how large an opportunity this could be, Microsoft has 300 million Teams users and 1.2 billion Office users. The mass corporate market will be the true honeypot for LSEG’s data – expect sales departments at both the LSEG and Microsoft to be frantically calculating how much they can charge large corporations on a per-user basis to access the LSEG financial data as part of their existing Office subscriptions.

Peregrine explained that this is not a distant relationship either. LSEG are working on the “inside”, directly with Microsoft’s coders and developers to improve the integrity of their internal technology infrastructure. Upon completion, Office-LSEG users will be able to “communicate both in and outside their organisation on Teams while sharing financial data in real-time, XMLs and PowerPoints will update automatically, the chat will be read by AI, and relevant information will be fed into the chat in real-time,” explained Peregrine.

AI winners?

AI is only as good as the data it’s fed. Fortunately, LSEG’s data is the gold standard for capital markets.

The group’s databases connect to 530 exchanges globally, they employ 7,000 experienced data experts to clean and audit the data, and because LSEG works with the capital market’s leading institutions, the outflowing information is perfectly positioned for AI processing as banks are programmed to accept data in the LSEG structure.

These factors, in combination with LSEG’s 30+ years of data management experience, led Peregrine to surmise that they “put us in a very good position to be a winner in AI.” And if current trends are anything to go by, the AI winners may well become the market winners.

Fierce competition

The financial world is defined by competition, and the battle to corner the “new terminal” market will undoubtedly be similarly competitive. LSEG’s deal with Microsoft will have spooked their competitors in the financial data delivery space who will be considering how to respond to this threat to the industry status quo.

However, LSEG’s competitors will struggle to partner with a company as ubiquitous or with the technological might of Microsoft. LSEG is already performing well: they make £3.5bn EBITDA, possess a market cap of £44bn, and returned £1.5bn to shareholders through buybacks over the last 18 months. It’s also one of the “best-performing stocks on the London Stock Exchange in terms of financial delivery in the last 20 years,” according to Peregrine.

As the race to democratise financial data consumption and access hots up, you’d certainly be tempted to place your bets on the current front-runner.

On the subject of oil,Washington has eased sanctions on Venezuela in return for free elections. The bonds more than doubled this week as American investors became free to buy them when previously they were banned.

We have therefore arranged a call with sector specialists including Elbek Muslimov from FPP Asset Management, which runs a fund that invests in Venezuelan bonds and manages investors’ claims.

The call will be held on Tuesday and we will discuss what happens next and whether we will likely see Venezuelan bonds double again.

Feel free to register here – it should be a fascinating discussion.

Carl Icahn sues Illumina

An interesting opportunity is brewing here: the company has had some real problems of late, with Icahn being just one of these issues. The company is facing large fines for the “forced acquisition” of $8bn Grail, which it is now being forced to sell.

I think Grail is worth a tonne of money when it is IPO’d or sold, but we will need to sit quietly and wait for the time being.

The underlying business is the world’s biggest genomics company, and as the Oxford Nanopore deal showed this week, the genomics theme is alive and kicking.

Nokia

A bit of a bloodbath for old club favourite Nokia this week as the company cut 14,000 jobs.

Blaming slow 5G rollout and a 70% drop in Q3 profits, the company hopes the cuts will save over $400m. We could be in the midst of a period of uncertainty for the telecoms sector as Nokia’s news followed Ericsson’s warning on Tuesday that uncertainty surrounding the telecoms arm of its business would persist into 2024 after reporting a fall in Q3 revenues.

Nokia’s restructuring probably represents an interesting longer-term opportunity.

In what is becoming a recurring theme (particularly for European investors), more bad renewable energy stock news came out this week as Q3 proved to be green funds’ worst-ever quarter for outflows.

Despite strong inflows in H1 of this year, renewable energy funds globally experienced a net outflow of $1.4 billion.

Some related news in copper markets this week as industry leaders warned that we simply will not have enough copper to go around in a few years’ time due to the lack of new mines opening. The strain this will put the EV (and wider renewable tech sector) under in a few years’ time will be immense.

The club held an interesting call on the state of the copper industry recently with Ivanhoe Mines who are seeking to address copper supply shortfalls by expanding their high-grade, high-volume Kamoa Kakula copper mine in the DRC and are conducting extensive exploration projects in the region – you can watch the recording here.

Without copper, there is no clean energy transition.

This reddish-brown metal – responsible for the progression of human civilization from the Stone to the Bronze Age 5,000 years ago – is facilitating society’s next giant leap as we aim to ditch 150 years of fossil fuel use in favour of an electrified energy system powered by renewable energy in a matter of decades.

With incredible conducting qualities bettered only by gold and silver (but at a far more affordable price), copper is the undisputed electrification king.

As a race against the clock to build batteries, electric vehicles, renewables, and electrification infrastructure emerges, combined with looming question marks about whether global supplies will keep up with rapidly increasing demand, the Curation Collective welcomed Marna Cloete and Alex Pickard from Ivanhoe Mines to understand more about the present state of copper mining and Ivanhoe’s upcoming projects.

A new copper hotspot

The Democratic Republic of Congo, long known for its vast mineral deposits, has recently become a major player in the global copper market. Up 17% compared to 2021, the DRC was the fourth-biggest copper producer in the world in 2022. The southern border with Zambia – an area known as the “copper belt” – is also now the centre of Ivanhoe’s copper operations.

It follows decades of political chaos and outright civil war, which is now beginning to subside – although pockets of conflict remain on the eastern border with Rwanda. There are several factors making the DRC an increasingly attractive proposition: the nation had its first peaceful transition of power following an election in 2019, its government is increasingly receptive to outside investment, a vast river network facilitates an abundant hydroelectric renewable energy system, and infrastructure is gradually improving, including an $850m road connecting Congolese copper mines to the Tanzanian capital Dar-es-Salaam. Plans for a $250m US-financed rail corridor from the DRC copper belt to the Angolan port of Lobito are also close to agreement.

Alex stressed the importance of the DRC as “global copper demand is expected to increase 82% by 2035. From our point of view, we have no idea apart from the DRC where that copper is going to come from.” Further Congolese copper discoveries are expected soon.

Kamoa Kakula

The jewel in Ivanhoe’s crown is the Kamoa Kakula mine, which Alex framed as “hard to contextualise how unusual this mine is.” Some of the mine’s statistics provide insight into Kamoa Kakula’s value:

It has the dual benefit of high-grade (5-5.5%) copper combined with high volume output (~600kT per annum by 2025) – an unprecedented combination.

One of the world’s greenest copper smelters will be completed in Q4 2024, powered entirely by hydroelectricity.

Ivanhoe expects serious returns on their early-stage investment ($2.9bn EBITDA in 2 years with a 65% margin).

Despite being a single mining facility, it accounts for 4% of the DRC’s entire GDP.

Ivanhoe also claims to be engaged in socially conscious initiatives at the facility, including a high rate of Congolese rather than “ex-pat” employees, the building of universities, and engaging in modern mining practices, unlike the now infamous manual, “artisanal” techniques used in informal copper and cobalt mines across the DRC.

The wider copper picture

Despite long-term outlooks for copper looking strong, it faces short-term hurdles in the market. The copper market is experiencing an extreme contango, where future contracts trade at a premium to the expected spot price, signalling weak short-term demand. It’s the first time copper has experienced this since 1994, with prices per metric tonne hovering around the $8,000 mark currently, down from the over $10,000 peak in March 2022 amid faltering demand and accumulating inventories. Additionally, a copper supply surplus is expected next year, driven by high output from new mines in Peru and Chile, followed by a significant shortfall predicted after 2027 as decarbonisation efforts accelerate.

The wider renewable market has also been wavering of late. It fits into a trend countering assumptions that renewable energy and technologies will experience uninterrupted growth as share prices dropped 20% across European markets in September amid rising interest rates and increasing material costs – impacting both renewable tech and renewable energy projects. Renewable energy funds also experienced a record net outflow of $1.4bn in Q3 2023 – a dramatic drop from the net $3.4bn added to renewable funds in the first half of the year.

However, Alex and Marna appeared confident that “world-class” Congolese copper will withstand these market fluctuations in the renewable sector. After all, it’s clear we need copper – not just for decarbonisation but also for facilitating rising living standards in developing nations – the main question is, will we have enough to go around? The medium to long-term copper picture looks far rosier than the present short-term uncertainty.

The mining sector has also been severely “undercapitalised” in recent years as investors flooded tech and healthcare markets with capital – the opportunity to enact meaningful ESG impact is significant in this frequently overlooked sector.

By 2035, 7% of the US population will be taking weight loss drugs like Ozempic – and food retailers are worried.

Walmart revealed that shoppers who picked up Ozempic prescriptions at their stores went on to buy less food during their grocery shop, while food manufacturers desperately scramble to formulate plans in response to the potentially 30% drop in calories millions of Americans will soon consume.

Will the supermarkets and restaurant groups find a way to profit over time or will this be a long-term battleground between appetite-suppressing weight loss treatments and food manufacturers/retailers?

Vacant office space: the new Airbnb model?

Right now, people see vacant offices negatively, so winning new space to manage is not seen as a real positive that drives revenues. The IWG narrative going forward needs to be about filling them up!

Empty houses are seen as a benefit to Airbnb because they fill them and clip the coupon. So, the equity story is all about increases in capacity utilisation from which Airbnb profits in a capital-light structure.

Until IWG get Worka up front and centre of their pitch and explains that it is the same model as Airbnb, people will not make the connection between empty space and filling it. In my opinion, Worka needs to be far higher up their list of priorities because it’s what makes empty offices a good thing in people’s minds.

Their marketing is also ineffective. They have no TV presence, so most people never see any of their ads – they are not investing in awareness, just saving every penny they can. People need to understand they get significant benefits through hybrid working with IWG (gym, healthcare, etc.)

IWG’s current thinking is as follows: the more offices they have and the bigger they become, the more people will appreciate their scale. However, people simply do not think that way, in my personal opinion.

We often talk about catalysts and there is unlikely to be a more important one than the return of the Victoria’s Secret show this fall as the stock trades close to all-time lows. Whether this brand has been lost in a celebration of diversity and can now get itself back on track in a tough retail environment remains to be seen; but as a catalytic event, it’s going to be an important few months for a retailer that for many has lost its identity.

CEO, Martin Waters, said that when the current management team took over running the company they “defined the challenge as being a complete repositioning of the brand”. At the centre of this is the reimagination of “probably the most important retail marketing device of the last decade in the Victoria’s Secret Fashion Show.” This quote in the FT gives you an idea of how seriously they are taking the relaunch.

Watch Amazon’s trailer for VICTORIA’S SECRET: THE TOUR ’23here.

Delivering Clinical Sequence Analysis in Under 60 Minutes – Oxford Nanopore & Oracle

Oracle Cloud infrastructure can now develop and deploy cloud-based sequencing applications which can analyse genomic data from large cohorts of patients. It’s hoped these new insights can shed light on the genetic causes of disease, aid the development of new diagnostic tests, and facilitate rapid treatment formulation.

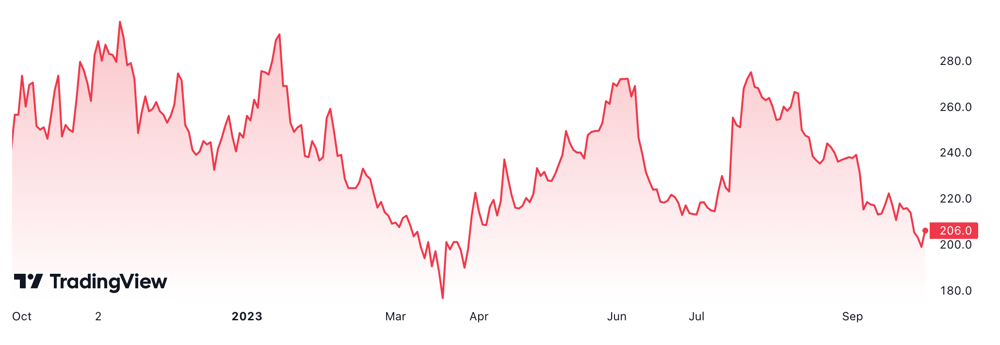

ONT 12-Month share price Source: TradingView

Yellow Cake

The uranium investment firm raised another £100m to buy Uranium and stick it in a vault! It’s interesting that they are still happy to do so after the recent price rises.

So although the shares may suffer some short-term indigestion, it should be long-term positive for the spot uranium price as more U308 gets stockpiled and taken off the market.

COVID showed us we could propel a drug from conception to market in less than 12 months. How many lives would be saved if we could do the same for cancer, diabetes, or Parkinson’s?

These are a few of the (at present) speculative medical questions e-therapeutics (ETX) are looking to find answers to.

As the only AI-focused publicly listed RNAi drug discovery company in the UK, the Curation Collective was excited to welcome Ali Mortazavi, CEO of ETX, to the club for an enlightening insight into AI’s role in medicine, the power of drug discovery platforms, and the future of clinical trials.

Demystifying drug discovery

Ali describes ETX as a “platform that is learning to compute the future of medicine.” “Compute” infers well-defined calculation, and, when combined with the “future of medicine,” ETX’s lofty ambitions become clear: to overcome the obstacles, high costs, and unpredictable nature of drug development with cold, hard computational and biological data processed through a reproducible methodological framework.

This framework manifests itself in ETX’s two proprietary technologies: the HepNet platform and the GalOmic RNAi platform. Together, they provide an end-to-end identification system of novel disease-associated genes and candidate drug therapies with disease-modifying potential.

The RNAi approach

The two most significant barriers to drug discovery (and lots of other things for that matter…) are time and money. Ali explained that the traditional method of drug discovery – the ‘small molecule approach’ – can, from inception to go-to-market, have a 5–7-year pre-trial timeline and incur costs of $25m-$115m. However, ETX’s RNAi approach has a two-year pre-clinical trial timeline, a $5m-$7m cost, and a far higher approval rate. Given it’s estimated that a massive 86% of drug candidates between 2000 and 2015 failed to achieve their stated endpoints, a more reliable, accurate approach is desperately needed.

It’s also worth noting that ETX focuses specifically on hepatocytes – a.k.a. liver cells in layman’s terms. In Ali’s words, this emphasis on hepatocytes is because the liver can be thought of as the “Amazon hub of the body” given its ability to distribute its output to almost every part of the human anatomy. Once Ali and his team were able to unearth a method of successfully getting drugs accepted into hepatocyte cells using computation, ETX had found a way to overcome drug acceptance in cells – one of the biggest hurdles to drug discovery – and achieving this in a cell type as influential as hepatocytes was a significant milestone for the ETX team.

Other innovative use cases of ETX’s technology include unstructured data patent mining, which can reveal new potential therapies users can then seek patents on, and the ability to design and predict mRNA sequences – with ETX’s technology able to interpret these complicated codes almost as a form of language.

The liberating effect this technology could have on the wider pharmaceutical sector is immense.

Transformative AI

ETX in its current iteration didn’t truly appear until March 2023. The catalyst? A “massive change in the performance of large language models (LLMs).”

Although Ali’s team had experimented with AI and LLMs previously, the upgrade in performance Ali noticed in these new generative AI systems models was so stark the ETX team came into the office the next day, had a meeting, and formulated a strategy to change “absolutely everything.”

The HepNet platform, for instance, went from a simple, search-oriented “Google for hepatocytes” to a troop of “mini AI agents” capable of being trained to become experts in specific medical fields, infer reason, and even self-code. From here, Ali described a scenario many of us will be familiar with from countless sci-fi stories:

“These agents can solve code. On a philosophical level, any form of intelligence that can code to improve its own DNA is a very powerful system…Now imagine these two agents stuffed to the brim with information, self-coding, reasoning, understanding, and then exchanging information with each other…in this sort of evolutionary process.”

Ali explained that his programmers don’t code anymore and would be better described as “architects” who design and manage the “AI agents.” The technology is so powerful that these architect-programmers engage in little practical coding because of the power of generative AI.

We no longer have to read a Philip K. Dick novel or re-watch Kubrick’s 2001: A Space Odyssey…the sci-fi future is already with us.

Humans are data

To continue on this sci-fi plane, Ali discussed whether the full clinical pipeline from drug conception to go-to-market could be done on a computer.

His answer – as you can probably imagine – is yes. And not just gene identification or sequencing – but also phase 1 trials, for instance. How? “Quite simply, human beings are data.” And once we have enough of this data stored within LLMs, we can begin to make accurate predictions about the effectiveness of drug candidates. This is not to say that real-world studies would become obsolete but that these could become pilots ahead of a full-scale AI-conducted trial.

Once this milestone is breached (pending FDA/EMA approval) and thanks to the incredible recent progress made in the generative AI and LLM fields “the future of medicine suddenly becomes very real”, observed Ali.

We recently highlighted that the psychedelic space was waking up after a year or two of hibernation. On Monday, we saw Cybin’s share price spike 40% after Proactive Investors flagged an SEC filing showing Steve Cohen’s Point 72 hedge fund had bought an 8.1% stake in the company. The filing date came two weeks after the publication of the results of a new Phase 2 trial which showed a single dose of psilocybin leads to significant improvements in people with major depressive disorder.

There is still a long way back for the shares which peaked at around $3 in the heady days of 2021 but the addressable market for depression is vast, so it’s definitely a sector we intend to keep an eye on.

Litigation Funding Industry

Major changes might be coming to the litigation funding industry following the news that the Supreme Court ruled many funding agreements as unenforceable. The Supreme Court holds that many litigation funding agreements should be classified as damaged-based so must comply with the applicable regulatory frameworks.

Pfizer’s Paxlovid is now less effective against Covid-19, a study suggests.

Remember we spoke about Atea in last week’s Wrap? This is interesting news for those following that company and the resurgence of Covid.

UK Housing Shortage

According to Bloomberg analysis, the UK Might Solve Its Housing Shortage by 2100. And while the UK’s housing issue is mired in political squabbling, the reality is that no matter how high rates get, people have got to live somewhere.

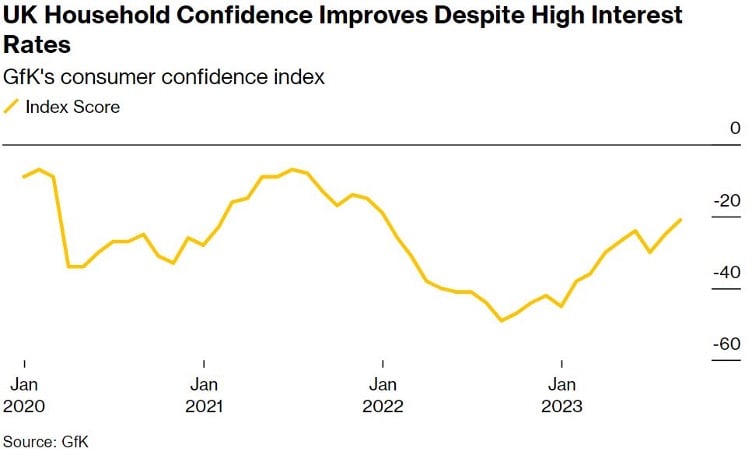

UK Consumer Confidence

Bloomberg wrote the following, which is borne out by M&S and Next’s strong profit figures as predicted by Savas when he spoke to us many months ago:

“UK consumer confidence climbed to the highest in almost two years as wage growth started to outstrip inflation. GfK’s sentiment index rose 4 points to minus 21 in September, the highest since January 2022. The survey found that British consumers are becoming more optimistic about the economy and their personal finances.”

Bloomberg goes on to say: “UK retail sales probably rose 0.5% in August, rebounding from the previous month’s 1.2% slide. Households have been willing to spend more and save less due to a relatively tight labour market…UK composite PMI is expected to edge up in September, while that of the euro-area is forecast to dip.”

Private members clubs for Manhattan’s uber-wealthy are thriving with competing clubs charging up-front fees in the region of a quarter of a million dollars. While these clubs can trace their roots back to 19th century London, it was Nick Jones who modernised the concept, launching Soho House on London’s Greek Street in 1995. Nearly three decades later, Soho House and its sister brand have more than 40 locations worldwide and are stepping up the pace of expansion, particularly in the US.

Although Manhattan’s new breed of ostentatious clubs will prove to be elusive for all but the top 1% of the population, Jones has succeeded in selling exclusivity to the masses while gathering a portfolio of trophy assets and we think it is only a matter of time before the company produces a decent return for investors or gets acquired.

The Inflation Reduction Act and renewable energy

The Inflation Reduction Act seems to have the opposite effect of its title by causing rampant cost inflation and supply chain disruptions to the renewable energy industry by boosting demand. An opportunity is brewing as many renewable companies entered unprofitable contracts, but more work definitely still needs to be done here.

We often talk about nuclear but the green transition will require a portfolio of solutions. If wind and solar falter due to poor economics it can only reinforce the need for nuclear power…although nuclear has a range of cost-related issues of its own.

If you saw the following information about the Vietnamese market, would you consider investing in its stocks?

2022 saw equity market capitalisation drop almost 35%.

“Problematic” real GDP growth in H1 2023 of 3.7% year-over-year, way below the ~6% growth typically experienced.

Vietnam has a frontier market classification despite some of its neighbours – including the Philippines and Indonesia – receiving emerging market status and commensurate fund inflows.

However, the scene could be set for Vietnam to join the emerging market club. The Curation Collective recently welcomed Dominic Scriven OBE, Founder of Vietnam’s $5.5bn AUM Dragon Capital fund management firm, to explain why Vietnam is such an alluring proposition for potential investors.

“Friends of everybody and allies of nobody”

Given its proximity to and similarities with China, it’s almost impossible to consider Vietnam without thinking about the global superpower positioned just next door.

Vietnam is the economy most exposed to a Chinese recovery, and China is its largest trading partner. Dominic described the volume of trade between the pair as “enormous” and predicts that despite Chinese economic forecasts routinely being downgraded in recent months, any pick-up in the Chinese economy will have a disproportionately positive impact on the Vietnamese economy.

But it is not just about China. Dominic described Vietnam’s approach to diplomatic relations as being “friends of everybody and allies of nobody”. Given our call with Dominic took place over a month ago, his comments eerily foreshadowed this week’s news of Biden’s visit to Hanoi to deepen diplomatic and investment relations between the US and Vietnam as the US seeks to establish an Asian manufacturing alternative to China amid souring relations between the two superpowers. Intel and Apple are already diversifying their supply chains by investing in Vietnamese facilities and the global semiconductor “Tech Cold War” will also undoubtedly play a role in US-Vietnamese relations.

As Vietnam hedges its bets between the two largest global economies, it could find itself in the enviable position of cordial diplomatic relations and robust trade agreements with both players.

Under the radar

Modern Vietnam, according to Dominic, only really began in the late 1980s with the passing of its first foreign investment law in 1989. After decades of conflict with colonial France, the US, and indeed with China in the late 1970s amid strict communist rule, Vietnam took longer than others to place itself in a position to accept foreign investment and administer a functioning system of corporate governance.

As a result, Vietnam still finds itself off the MSCI’s list of emerging market economies despite exhibiting many of the qualities found in these markets, such as rapid industrialisation, urbanisation, and market capitalisation that has more than quintupled from an average of $30bn in 2012 to more than $150bn so far on average in 2023.

This ‘misclassification’ could turn out to be a positive characteristic for clued-up investors as Vietnam still fails to register on many investor radars. Due to its frontier market status, it is also viewed as a significant risk by many not aware of the favourable conditions present in the Vietnamese market.

Dominic predicts an upward reclassification to emerging market status in 2025, undoubtedly bringing an influx of interest and fund flow.

A discount trade

If we come back to some of the “unfavourable” characteristics listed in the introduction of this post, the underwhelming few years experienced by the Vietnamese market may provide further benefits for savvy investors as Dragon Capital shares trade at a 13% discount to NAV due to Vietnam’s tricky 2022 and rocky start to 2023.

While sluggishness may continue, Dominic foresees a growth-catalysing cocktail of lower interest rates, rebounding tourism levels, and government incentives steering Vietnam back on track in H2 of 2023 and into 2024 – an assessment backed by other financial analysts.

Don’t judge a market by its cover

Whilst Vietnam’s near-term performance figures may not get investor pulses racing, it could provide the perfect conditions for great value-for-money returns in the medium to long term as many overlook Vietnam, chasing short-term performance elsewhere.

With Vietnam finding itself in a unique diplomatic position in the Chinese-US trade conflict, on the verge of an upgrade to emerging market status, and with favourable long-term growth drivers, now could be the time to jump the queue and invest in Vietnamese stocks before the investment floodgates open.

More evidence that small doses of clinically administered mind bending drugs can materially improve your mental health. A study published in Nature found that individuals microdosing psychedelic substances experienced “increased self-reported psychological well-being, emotional stability and reductions in state anxiety and depressive symptoms […] plus increases in psychological resilience, social connectedness, agreeableness, nature relatedness and aspects of psychological flexibility”.

Now, California are on track to become the third US state to decriminalise personal psychedelic drug use, following Oregon and Colorado – try explaining that one to the headmaster!

Blackrock-led consortium off-load a big chunk of stock

In a busy week for a normally sleepy company, 36 million shares of LSEG changed hands when the Blackstone-led consortium that sold Refinitiv to the exchange operator reduced its stake for the third time this year. Since swapping Refinitiv for a 37% stake in the LSEG in early 2021, shares in the group have traded in a fairly tight range. The latest deal, which included the sale of 9.5m shares to the LSEG, leaves the consortium with a voting interest of about 12% holding. This is subject to a 180-day lock-up. While the consortium still holds this stake the cap on the share price probably hasn’t been removed just yet, but it doesn’t feel like there’s a lot of downside risk, particularly given the latest wave of interest in data prompted by the launch of ChatGPT last November.

LSEG also led a fresh funding round for Nivaura, a start-up it first backed in 2019. Nivaura’s aim is to tokenise traditional financial instruments. It pioneered the issuance of regulated bonds on blockchain in 2017.

Finally, LSEG announced a move to enter the private equity space via a strategic investment in Floww, a platform that connects start-ups with funding partners, a deal that follows Deutche Börse in partnering Forge Global support its entry into European markets.

New hire at Illumina

The unenthusiastic share price performance of Illumina following Jacob Thaysen’s appointment as CEO has been attributed to his lack of experience in a similar role. However, with the full backing of Carl Icahn, we think his appointment could be the catalyst of a turnaround.

This week, it was confirmed that M&S will return to the FTSE 100 when the index conducts its next quarterly reshuffle, four years after it dropped out.

This is one the club got right – it’s nice to see it back where it belongs.

Rolls Royce Renaissance

Another UK company experiencing something of a rebirth this year is Rolls Royce.

Despite being 150% up in the past year, UBS upgraded its price target from 200p to 350p and said the price could reach 600p in a best-case scenario – a near threefold increase.

The shares have been trending higher since it surprised investors with a sizeable hike in forecasted profits following growing demand in its jet engine and defence businesses this year. And all this happened before the potential benefits of its small modular reactors materialised.

This week, the company announced that it has broken ground on Beijing Aero Engine Services Company Limited regarding the maintenance, repair and overhaul facility that is expected to go into operation in 2026. This is a 50/50 joint venture with Air China.

Oil for Debt or Oil for Food?

If you have never read “The World for Sale” it provides a fascinating insight into the world of commodity trading over the last 50 years and explains how today’s mining and commodity giants were born in faraway lands. It’s a great read.

This week Repsol and ENI were both given clearance by the US State Department to help ease Venezuela’s gasoline and food shortages in what is being called an oil-for-debt swap – in reality, it may in fact be an oil-for-food swap or access to certain foreign products in exchange for increased crude oil shipments to Europe.

This follows reports last week that US officials were drafting a proposal that would ease sanctions on Venezuela’s oil sector, allowing more companies and countries to import its crude oil on the condition that the South American nation moves toward a free and fair presidential election.

More to come on this later in the year and how we might profit from Venezuela’s sanctions being eased.

Pot Stocks Fly Higher

We highlighted a few weeks ago that marijuana stocks had been somewhat forgotten. This week saw a surge in pot stock share prices after reports that US health officials had recommended easing restrictions on the drug.

Early days but let’s see if this trend has legs.

The problem with climate change policy

The problem with implementing climate change policy – explained beautifully by Gerald Butts is as follows –

“The US blames Chinese and Indian coal plants. China blames Western colonial history, whilst Africans and Indians assert their right to develop their economies as Westerners did.”

Semiconductors are the world’s most powerful, ubiquitous, and contentious translators.

The tiny silicon “chips” – which interpret and process the binary language of 0s and 1s that power all computational devices – facilitate the operation of our digital-first civilization, are buried deep in almost every electrical device you own and are now engendering a “Tech Cold War” between China and the US.

Tension has been building for years, but recent directives have brought renewed focus on the steadily escalating trade war:

In October 2022, Biden announced semiconductor export controls to China, citing Chinese use of semiconductor technologies for military purposes.

August 2023 saw US investment restrictions on Chinese AI, semiconductor, and quantum information technology funding.

The tit-for-tat sanctions reverse years of increasing global economic integration, signalling an era of increased protectionism, deglobalisation, and regionalism as supply chain pressures mount.

Four key actors operate in the fragile, interconnected semiconductor space, all of whom play distinct roles: the US (chip designers and researchers), China (importer of chips to satisfy its huge electronics market), Taiwan (the silicon “foundry” of the world), and the EU (the jack of all trades, involved in all aspects of the semiconductor value chain.)

However, China is now accelerating its transition towards producer rather than importer of chips, throwing this delicate industrial ecosystem into chaos.

Within this intricate geopolitical context, the Curation Collective recently welcomed Thibault Morel and John Klein from European investment bank Bryan, Garnier & Co. The pair shed light on the state of this critical industry, which acts as a petri dish for many of 21st-century society’s developing themes and trends, as they considered the trajectories of two European semiconductor players: STMicroelectronics (STM) and Infineon Technologies (IFX).

An import-ant shift in China

Since Xi Jinping announced the Made in China programme in 2015, the Chinese economy has looked to pivot from being a low-end producer reliant on foreign imports to an independent, advanced manufacturer of cutting-edge technologies.

Consequently, domestic semiconductor production is expanding rapidly, aided by generous state subsidies. China’s rejection of its role as chief importer is causing concern among EU semiconductor firms – Thibault estimates that China now accounts for 12-13% of market share, rising to 20% in 2025, with growth accelerating further in the following years.

Less demand from China ultimately means more competitiveness among non-Chinese firms as their addressable market tightens.

Funding gaps

EU firms are also hamstrung by lower funding than their US and Chinese counterparts: in 2022, US firms were given $280bn in government subsidies, the Chinese figure was $143bn, while EU subsidies were dwarfed at just $33bn. EU firms are also only awarded 1-2% of their sales in grants, while some Chinese firms received a massive 40%.

Chinese subsidy allocation directly competes with the EU too. Both economies focus production on mature (i.e. less sophisticated) rather than advanced technology chips, further squeezing the bloc’s market. In contrast, the US allocates subsidies to advanced chip production used in innovative tech like AI.

Further funding disparity occurred in innovation investment – China accounted for 60% of total innovation funding, and the EU just 10% of the $20bn raised between March 2022 and May 2023.

Contrasting Fortunes

IFX and STM are not in an easy position. They sit in the centre of a geopolitical storm, are experiencing significant market contractions, and face unprecedented supply chain pressures. Despite this, Thibault and John foresee diverging futures for the pair.

Although both face significant disruption from Chinese domestic semiconductor growth, Thibault sees IFX as a safer bet because:

IFX has a homogenous, industrial-oriented portfolio. Greater focus has allowed IFX to position itself as an industry leader in the power discretes and high voltage module niche, with a broad range of customers, including in the growing automotive market. They have also acted pragmatically and outsourced some manufacturing capacity to TSMC in Taiwan.

Whilst STM’s revenue growth is driven by automotive and industrial, it is more exposed to the highly competitive consumer electronics market which has delivered declining revenues for the firm. In addition, STM has a high customer concentration.

Thibault predicts that IFX will “resist attrition of the addressable market”, gain larger market share in Western economies as Chinese independence grows, and forecasts a 15% upside on IFX shares compared to a 30% downside on STM.Despite Thibault’s confident predictions, the fragile semiconductor ecosystem will undoubtedly be disrupted again, potentially undermining his predictions. It will be fascinating to see how the industrial and geopolitical situation develops in the months and years ahead and how the tensions – and indeed incidents of industrial cooperation – impact wider society.

Lateral thought – “Tour de France” streamed on Netflix

In share price terms, few companies benefited more from the pandemic than Peloton, and its fall from grace has been equally staggering. Shares collapsed again this week – it would appear that buying $2,000 gym bikes no longer feels like a top priority for most people.

As someone who has historically hated cycling (both watching it as a sport and participating because I find saddles don’t agree with my backside), I was blown away by the power of the new Netflix series “Tour de France.” I never really appreciated quite what these guys endure and how close to death they can come.

I wonder whether this series might do to Peloton what Drive to Survive did for Formula 1. If Peloton is to be saved, it will need some external help once again.

Burford Capital

The SEC finally signed off on the way Burford accounts for legal cases thus laying the foundations for a global standard in how to account for litigation finance.

Where are Muddy Waters now, with shares having doubled since we first drew it to members’ attention?

For those who care, Hexagon in Sweden has undergone a similar bear attack from a research boutique which we think has little merit. Uranium Energy Corp (UEC) shares also got smashed in yet another bear attack a few months ago and have also fully recovered.

My point here is that these types of bear stories can sometimes provide a great opportunity if the company ends up having a clean bill of health.

Nike

At the time of writing, Nike hasfallen for a record 11 sessions, erasing more than $13 billion in value following concerns over China’s recovery. There is lots of competition in this space nowadays and global brand ambassadors are no longer the sole preserve of Nike.

It’s a great stock, but it’s not cheap and faces multiple headwinds. Alongside Nike, it seemed like every US retailer – from Foot Locker to Macy’s – posted warnings last week.

The FT writes, “A boom in PwC’s Saudi-dominated consulting business in the Middle East helped the Big Four firm’s UK partners avoid a significant drop in pay last year as rising costs dented profits.”

Those subscribed to the FT can read the full article here.

We have been following consulting companies like Accenture and Cap Gemini closely and have wondered whether AI might provide a similar profit boom for the big consultancies going forward.

Obviously, Nvidia’s incredible numbers are at the front end of the curve, but what’s coming down the pipe may be less well understood.

The Gold Standard

The leaders from the five-member BRICS group of nations — Brazil, Russia, India, China and South Africa — are set to expand the bloc to include Saudi Arabia, Iran, Ethiopia, Egypt, Argentina and the United Arab Emirates in 2024. The expansion suggests the group harbours ambitions of becoming a geopolitical alternative to Western-led forums.

Why do we care? Well, it’s possible that we see a massive move in the gold price towards the end of this year as any move by the BRICS to provide a rival currency to the dollar seems certain to involve gold in some way, shape, or form. The World Gold Council intends to digitise gold and help people use it to make frictionless payments in their daily lives via a project called Gold247.

More on this later in the year, but the politicisation of the dollar in world markets encourages the creation of a new currency, so why not revert to the world’s oldest one using blockchain and a mobile phone?

Scarcity remains one of the world’s greatest commodities – gold always has that going for it!

China has the world’s largest overweight and diabetic population and could offer treatments at a lower price – will these Chinese-developed obesity drugs disrupt the wider weight loss market?

Argentina Primaries

Earlier this week, rightwing outsider candidate, Javier Milei, won a shock victory in the Argentinian primaries.

IWG results – Record H1 revenues reported by IWG on Tuesday were in stark contrast to WeWork, which reported a 21c EPS loss (13c loss expected) and warned its ongoing commercial viability was in serious doubt. Post a 38% decline in its share price on Wednesday, WeWork was valued at slightly more than 0.5% of its $47bn peak.

The key catalyst – During a post-results interview with First on CNBC, founder and CEO Mark Dixon reiterated the group’s mid-term plan to spin off its tech business Worka, described by Dixon as the “picks and shovels” of hybrid working. These comments, which went largely unnoticed, highlight a key catalyst for unlocking real value in the group.

Commodity super powers – It’s amazing how little we read about the DRC, Indonesia and Chile given their vital role in the energy transition. We are trying to track people down to speak to the club. Full insight available here.

The obesity crisis – A big news week for Novo Nordisk, which started off countering recent headlines about negative side effects from its weight loss drugs when it released headline data from a five-year, last stage trial of 17,604 overweight / obese adults aged 45+ in 41 countries. The trial revealed a 20% reduction in the risk of serious cardiac events in people given Wegovy with the better-than-expected outcoming prompting analysts to say that this will likely help persuade more healthcare providers and insurers to fund the drug. Martin Lange EVP of development said it has the potential to fundamentally change how obesity is regarded. This also gives Novo a four-year head start on Eli Lilly’s SURMOUNT-MMO trial which is not expected to read out until Q4 2027.

The company also reported H1 sales of DKR 108bn ($16bn), + 30% and in line with expectations. Sales of obesity care products more than doubled but were slightly below estimates. However, Novo raised sales growth forecasts to 27-33% (from 24-30%) and said it expects operating profits to reach 31-37% (from 28-34%). Novo also announced it is investing DKR 25bn ($3.7bn) to expand its manufacturing capacity to address supply chain bottlenecks.

Finally, Novo announced it has agreed to buy Inversago Pharma for up to $1.075bn – subject to development and commercial milestones – acquiring new therapies in development that include a range of treatments for obesity, diabetes, complications associated with metabolic disorders and kidney disease.

Illumina – cut annual profit forecast in a sign that a funding crunch among its biotech and pharmaceutical clients is expected to weigh on sales for its genetic testing tools and diagnostics products.

Shares have fluctuated, down by as much as 6%. The company is probably kitchen sinking the numbers ahead of a change of management and quickly recovered their ground. Long term we still like this area as gene sequencing entire populations is a way of fixing broken health services.

Apple Numbers – can you bank on them or with them going forward?

It’s not easy to move the needle on a three trillion dollar market cap company and there just aren’t too many markets that are big enough for Apple to dominate and materially impact earnings.

Results last Thursday were reasonably tame with much of the growth coming from services. As I mentioned in last week’s note, it’s their banking ambitions that interest me most: Apple has said that its 1 billion service subscribers have deposited more than $10 billion in the last few months into its savings account that is on offer in partnership with Goldman Sachs.

LLM + CC + BS + BL + 4% + iPhone = The end of banking as we know it.

AI-driven LLMs at the front end + a vast balance sheet + a credit card + a banking licence + 4% yielding current account + the ability to acquire or copy the world’s best challenger banks’ software inside an iPhone (that has already become your wallet), may be the most disruptive thing to happen in the history of the banking world.

Take a look at the simultaneous demise of PayPal shares, whose earnings continue to disappoint investors.

Mass consolidation of US regional banks is probably on the way and possibly more bank runs here folks if this goes where I think it’s going. Imagine Revolut being owned by Apple and that’s where my head is at…watch this space.

Cameco

The long-term thesis on nuclear remains intact but despite the recent coup in Niger (representing 15% of the EU’s uranium requirement) the uranium price remains stable. Cameco will shortly become an integrated uranium play, shifting away from pure mining which does change the company’s dynamic somewhat. However, what caught my eye was that the average sale price was still well below the cost of production. The shares will need a big pop in the spot price of uranium to move it materially on from here after a great start to the year.

London Stock Exchange

Results were slightly below consensus, but the real story remains how the company’s relationship with Microsoft unfolds as the two learn to mine Refinitiv’s curated data set. LSEG will host a capital markets event on 16th and 17th November, during which investors will have the opportunity to quiz management on the business.

Two new names for us to follow – Upwork and Fiverr

Upwork Inc. (UPWK), along with Fiverr (FVRR), dominate the freelance employment platform market in the US. Freelancing has been on the rise for many years and exploded during the pandemic, but unlike many other businesses, the pandemic seems to have cemented these two companies’ position rather than simply giving them a short-term pandemic stimulus. Both had good results last week and both are names to watch in a world where working freelance is the natural beneficiary of the post-Covid employment world.

When Anthony Chow, Co-Founder of Agronomics – one of the cellular agricultural sector’s only publicly listed vehicles – explained to the Curation Collective, “think of it like the energy transition: we continue to need fossil fuels, we need solar and wind, we need nuclear. We also need every means possible to produce protein,” he revealed how imperative Agronomics’ influence may be on the future course of human society.

Consider our most pressing societal issues: water consumption, greenhouse gas emissions, food security, ocean sustainability, pandemic prevention… Agronomics’ portfolio of businesses ranging from precision fermentation facilities to cultivated leather, could mitigate these threats to some degree.

For example, studies predict that cell-cultured meat could have a 92% lower carbon footprint than current industrialised beef production if powered by renewable energy sources and be three times as efficient as industrialised chicken production – the most efficient means of industrialised meat production – in terms of land use, air pollution, and other environmental factors.

Agronomics’ potential market is inconceivably large. In a scenario that seems a fantasy now but may become reality in a few decades, cellular agriculture could usurp traditional agriculture as food security and sustainability themes likely become of growing importance. Even by 2030, projections suggest the cultivated meat market could reach $25bn.

However, laying the practical groundwork for this radical transformation in society’s relationship with agricultural production is proving challenging. The infrastructure for creating cultured protein is scarce: fermentation capacity will require a 100-fold increase over the next decade to keep up with market growth projections.

The initial steps towards scaling infrastructure are coming with the first large-scale US facility in construction by Agronomics’ Liberation Labs in Indiana. It will host 80% of all precision fermentation processes and have a capacity of 600,000 litres – enough to produce 500-1000 tonnes of dairy or egg protein per year.

Agronomics’ next obstacle is that cultivated meat will only saturate the market when price, taste, and convenience match standard meat products. Using current cell-culture technology, it would cost $1.8tn to produce 10% of global protein, according to Anthony. Therefore, a large “green premium” would initially be attached to cultivated meat products.

In terms of taste, cell-cultured meat is chemically identical to conventional animal products, which should help it overcome the sales stagnation experienced by plant-based meat substitutes that have struggled to replicate the taste of their animal-derived counterparts. However, a narrow product portfolio limited to unstructured products such as mince and burgers currently corners the cell-cultured product offering. The tide may be turning here as the FDA has approved lab-grown chicken made by Upside Foods and Good Meat to be sold in the US. Agronomics also expect regulatory approval for its cellular aquaculture firm Blue Nala in Japan next year.

Another barrier to overcome is consumer scepticism. Lab-grown meat may raise health and nutrition worries for some consumers and Anthony argues that consumer education is essential to counter these concerns. The unique benefits, such as minimal disease exposure compared with conventional farming, must be emphasised.

Agronomics’ share price is down more than 72% since its peak in 2021. Scarce infrastructure and the lengthy timeline until commercialisation have hampered its progress. Despite the challenges, Anthony is highly optimistic about Agronomics’ pipeline and the recent strides to bring cell-cultured meats into the general consumer space. Agronomics is trading at 5.8x current year annualised earnings – a 48% discount to the FTSE All Share Index.

Agronomics may be one to invest in now and leave on the back burner. Don’t expect to see any major returns for a few years yet but when they come, the returns could be game-changing.

Portfolio overview

Agronomics’ portfolio contains a total of 23 companies ranging from precision fermentation to cell-cultured leather:

Rolls-Royce shares surged after an upgrade in profit forecast. Shares rallied 25% after the firm upgraded guidance for FY operating profit by 40% to £1.2-£1.4bn – above the consensus of £934m.

We have been banging on about the airlines for a while now, so it was not too surprising the company that supplies them with spare parts and new engines would recover as well. This was on our one-to-watch list a few months ago.

Streets are getting so hot they are causing serious burns

Burn centres in the US southwest are reporting a rise in injuries to people who touch too-hot door handles, walk barefoot on scorching surfaces, or fall on sun-scorched pavement.

Melting infrastructure is another massive problem and opportunity as the world burns and becomes increasingly uninsurable. There will be much more on this in the weeks that lie ahead.

Meanwhile in Europe, dairy farmers are using giant fans and sprinklers to help their cattle cope with extreme heat.

UK Supreme Court deals blow to litigation funding industry

The Supreme Court’s decision will send shockwaves through the industry and affect other civil lawsuits that have similar litigation funding agreements in place, lawyers say.

We have reached out to Burford for a response and will report back to members in due course.

The DNA/RNA specialist reiterated guidance for the full year as shares rallied 20%. This is not only good news for Nanopore but should put a firm base under the shares of IP Group that still trades at a very steep discount NAV, and still owns a 10.1% stake in Oxford Nanopore.

Macquarie takes further control of Britain’s gas network

This week an investor-consortium led by Macquarie, the world’s biggest infrastructure asset manager, moved closer to taking full control of National Gas, increasing its stake (by 20%) to 80% and acquiring an option on the remaining 20%. The move comes after National Gas and the other four UK gas grid operators committed to mixing hydrogen with the gas in Britain’s main pipelines by 2025, earlier this year. Similarly, Germany’s government is working on a revamp of its national hydrogen strategy with the final draft due to be approved this month.

Hydrogen stocks around the world have been warming up recently and this deal seems to ensure the longer future of the entire constellation.

Microsoft to charge $30 per month for generative AI features

Microsoft announced it will charge $30 a month for generative AI features, a more than 50% premium on the price for Microsoft 365 without the AI bolt-on.

CEO Satya Nadella defended the pricing decision as part of a generational technological shift.

This announcement temporarily sent Microsoft shares to even dizzier heights.

Whilst new LLMs seem to be a rather regular occurrence these days, we continue to believe that the real money is going to be made by attaching them to data sets that are then mined to produce valuable insights.

For example, having an LLM attached to Refinitiv or Bloomberg data would allow subscribers to ask a simple question at the front-end, whilst receiving deeply insightful answers from the back-end data. So, taking unstructured data and enabling an LLM to solve complicated issues by allowing anyone to ask simple questions is going to be the battleground.

We continue to follow the progress of both the London Stock Exchange and Bloomberg for this reason.

Imagine the scene: a few years ago, your investor calls were spent trying to drum up interest as pricing pressures, increased competition, and an inability to differentiate your products caused share prices to drop rapidly while your firm continued to report flat, single-digit growth.

But fast forward a few years: now, share prices are skyrocketing following the commercialisation of a “revolutionary” molecule. Forecasts predict a 30% top-line growth rate, and, despite your mega-cap biopharma status, your firm is attracting a “premium growth” label from sell-side analysts.

This was the scenario experienced by Mark Root, Director of IR at Novo Nordisk, as the discovery of the GLP-1 molecule propelled the Danish pharmaceutical giant from a steady plateau in the diabetes market to the zenith of the pharmaceutical sector following successful forays into obesity treatments.

The two products driving this growth – Ozempic and the newly released Wegovy – are FDA-approved, while Wegovy is available as part of a trial in the UK (although that’s assuming you can get your hands on a dose). Clinical trials show that users can lose 15% of their body weight – with the results improving markedly among younger people.

While Ozempic is already an established type 2 diabetes and off-label weight loss drug, Mark believes Wegovy offers the most significant growth potential.

According to Mark, “Obesity is a burgeoning market, and at Novo Nordisk, we see it as a chronic disease.” The potential for growth in the obesity market is extraordinary: last year, the company only treated 500,000 of a 988 million-strong addressable worldwide market, analysts predict sales of weight management drugs will rise to $30-50bn by 2030, and more accessible oral (rather than injectable) treatments are currently moving through trials. Considering these factors, a 20-30% sales growth forecast is well within reach.

So, will the good times keep rolling for Novo Nordisk? The obesity market is immense, but the issues that stalled its progress in the diabetes market may soon thwart its current ascendency. Increased competition, such as Eli Lilly’s progress in developing a GLP-1 pill, may limit its domination of the obesity market. Competitive advantage may diminish further as semaglutide patents expire as soon as 2026 in Brazil and 2030 in many other territories, while concerns over the treatment’s side effects may create hesitancy in the medical profession.

In addition to supply chain struggles in the UK, Novo Nordisk has warned of similar issues in Australia, Ireland, and Germany, where doctors have been urged to limit Wegovy prescriptions.

As adverse factors mount, only time will tell whether Novo Nordisk can maintain its extraordinary growth momentum.

Fat Gladiator Investment Club, recently rebranded as Curation Collective, held another in-person event, a “Future of Healthcare – Investor Forum”, this time at the UnHerd Club in Westminster.

Without a spare seat in the house, the afternoon was full of surprising facts, enlightening discussions, investible ideas and the occasional point of contention. The evening, on the other hand, was an opportunity to network with the other members and learn more from the presenters. A digital copy of the day’s prospectus is available here.

At its core, the Curation Collective is an elected professional and high-net worth investment club with a dream of democratising access and investible outcomes to everyone. As such, Curation Collective has a freemium offering, where investment ideas and videos are posted regularly. Sign-up today!

And with that in mind, we’ve outlined the key takeaways from three of the most interesting companies that presented.

The End of Organ Donations – Tissue Regenix [TRX]

Tissue Regenix is a publicly listed, sub-£50mn market cap health-tech innovator. CEO Daniel Lee, sat on our second panel, entitled ‘Innovations in Health-tech’ to tell us about the incredible strides the company is making in regenerative medicine.

Every year, 225,000 heart valve replacement surgeries are performed. Regenerative medicine, an interdisciplinary field which can invole stem cell therapy or tissue engineering, aims to alleviate the economic pressures of immunosuppressant drugs, examinations and multiple operations, eventually removing the need for organ donations altogether.

The online version of the UK newspaper The Telegraph recently ran the striking headline “Single blood test picks up prostate cancer in 100 per cent of cases” (Laura Donnelly Health Editor 25/02/23). The story looks at the rapidly evolving science around ‘liquid biopsies’ – non-invasive testing that provides real-time information about the presence of tumours and their condition. This offers significant potential for mass screening and early detection across an array of cancers.

It emphasises, yet again, the vital importance of societal focus upon, and investment in, the advancement and acceptance of preventive medicine.

As we know, around the world, healthcare systems are struggling, and in many cases failing . The challenges being presented by the intensifying healthcare demands of growing and ageing populations are simply too vast. It is obvious that extensive increases in access to, and education about, preventive healthcare solutions will drive deep and long-lasting improvements.

Far too many of us have been personally involved in situations where early and accurate screening either have or would have, had life-changing consequences. This is particularly true within the cardiovascular and cancer conditions, the highest causes of early death.

“Prostate cancer is very treatable if caught early, but too many men are still diagnosed too late, when their prostate cancer is incurable – which is why we urgently need a screening programme” (Simon Grieveson – Prostate Cancer UK)

Across our Curation and Fat Gladiator Investment Club platforms, we continue to identify, track and draw focus to some of the technologies, sciences and companies which we believe are at the vanguard of the solutions.

We introduced our members to IP Group – the £675mn market-cap FTSE 250-listed entity dedicated to finding and developing great research ideas into world-changing businesses. Amongst their life-sciences portfolio is Genomics plc, spun out of Oxford University and is making strides in enabling all stakeholders within the provision and receipt of healthcare to benefit from better application of genomics science – the science that lies at the core of liquid biopsies.

“Together, we are working towards a world in which we can understand the mechanisms of disease well enough to produce effective and tailored medicines, and one in which we routinely identify and target those people most at risk of all the common and chronic diseases” (Professor Sir Peter Donnelly CEO Genomics plc)

Preventive medicine will be one of the key themes of our Future of Healthcare Investment Forum being held in London on April 26th . This forum will connect panels of sector experts and company managements to expose and debate the innovations and investment opportunities that are transforming health provision.

One of the companies attending the forum will be Echelon Health – with whom we have been in partnership for two years. Their comprehensive assessments can detect diseases that lead to premature death in up to 92% in men/95% in women. Their combined deployment of clinical expertise and the most advanced screening technologies currently available have made this possible. We have first-hand experience from employees and members whose lives have been saved by Echelon’s imaging capabilities and expert analysis.

Echelon Health provide a significant discount to any of our employees, members and their families who wish to engage them. We are delighted to say that their team will be presenting on Monday 6th March at 17:30 and recipients of this communication are cordially invited to register here to learn first-hand about what they do and, if you choose, to benefit from the Curation and Fat Gladiator discount.

“Africa’s story has been written by others; we need to own our problems and solutions, and write our story” (Paul Kagame, 2013)

The Curation and Fat Gladiator Investment Club platforms track all sorts of companies, in all sorts of geographies, for all sorts of reasons. Our favourites are the ones that we follow simply because of what they stand for – the ones that inspire us. Buzigahill is a fashion venture in Uganda. It is writing a masterpiece. In the 1970’s, the country was famed for its vibrant fabric and garment production. The tsunami of cheap second-hand clothing coming from the Global North extinguished a flame that had burnt very brightly during dark times. Bobby Kolade lived for many years in Uganda, before heading to Europe and establishing a successful fashion business. Mr Kolade has returned home – and is sourcing items of second-hand clothing from the markets in Kampala and Owondo. Those items then undergo transformational design in the hands of a team of local seamstresses – before being offered for sale on the Buzigahill website as unique items of fashion (each with its own “passport” of provenance), back to people in the very countries from whence they came in the first place.

“We’re trying to say, we can do more here than just consume your waste. We’re creative, we’re resourceful, and by purchasing this item you are helping to build an industry that your industries have not quite contributed to the development of.” (Bobby Kolade)

And the name that appears on the labels of each item emerging from this beautifully pure example of the power and importance of circular economies? …. “Return to Sender”.(see: ABOUT BUZIGAHILL – BUZIGAHILL) and (Return to Sender: Bobby Kolade’s new collection) Uganda is one of the 11 African countries in which our friends at Jumia continue to write their particular story, and last week, our members met with Francis Dufay, the recently appointed CEO. Jumia’s core business is Jumia Marketplace – connecting online shoppers with a wide range of sellers of apparel, smartphones, electronics, beauty and homeware products.The company has often been referred to as “The Amazon of Africa” – a title about which Francis was characteristically straightforward – he absolutely loves it when he hears it, but stresses that Jumia is a very different business, being built in very different circumstances. In the simplest of terms, its all very well building an online marketplace for consumer goods – but it will only work at scale and profitably, if the infrastructure exists that enables the goods to be moved and paid for. That is a very different prospect in 11 countries in Africa. An African company is having to write its own story – in this case, the building of Jumia Logistics and JumiaPay alongside the core platform. Jumia faces significant challenges – the inflationary macro conditions are impacting supply chains and consumer firepower. There have been understandable concerns around cash runway, and those are still relevant – but Francis was reassuring about the scale and depth of the recent cost-cutting and organisational restructure programmes. The Economist Intelligence Unit predicts an ebbing inflationary tide across the region in 2023 – fingers crossed, because what we do know is that Jumia is potentially a great play on the consumer activities of a growing, young, commercially savvy and urbanising population who are living in era of rapid growth in internet and smartphone penetration. Finally, whilst it is invidious to seek to make too many direct comparisons with India’s explosive consumer growth – it would be equally unwise not to give weight to some of the clearly visible streams of commonality. Hence, this week, our members are having a call with the team at Gaja Capital to explore investment conditions and opportunities in India – and part of our focus will be on identifying the areas where the lessons of their history can be exported into our tracking of the investment themes in Africa.

With the global economy running low on growth drivers, once again India is being tagged as “the next big thing”. We have been here before, and there are legions of corporates and investors who have been right about the fundamentals, but who have, all too often, ended up foiled and frustrated. The refrain has tended to be about the wonders of the country and its people, but the impossibility of doing business there. Gopal Jain is the founder of Gaja Capital and he met with our members this week. Gaja is a leading Indian Private Equity Fund, established in 2004. Gopal was inspired by his mother – who made the decision to stop work, to take her savings and to focus on supporting the family by trading the stock markets. “I won the lottery of life with my parents…” says Gopal, who made his first investment at 13. He sees India’s growth being powered by “The Four D’s” of Deglobalisation; Digitalisation; Decarbonisation and Demographics. He sees that:

“By the end of the decade, India will not only be the office, but also the factory of the world.”

Gopal was compellingly bullish on the power and sustainability of the current growth phenomenon – and we would recommend spending time on the Gaja website to see the types of companies that are flourishing. Gopal is far from being alone. A recent report from Morgan Stanley sees GDP growing from $3.5 trillion today, to $7.5 trillion by 2031. They make the point that India is one of only three economies capable of generating more than $400 billion of annual economic output growth from 2023 onwards, rising to $500 billion after 2028. They join the growing list of believers that India will be the third largest economy by 2027, and will have the third biggest stock market by the end of the decade. As Nandon Nilekani of Infosys puts it:

“People are looking at which other place over the next decade is going to be a great place to put capital. I haven’t seen this kind of interest in India for 15 years”

What we find most interesting – and most compelling – is the stuff that is happening at ground level. It is very redolent of the “incremental gains” theories espoused by successful sports coaches. If we are right, these are the kinds of things that will make the real difference. Narendra Modi became PM in 2014 – and whilst he will always generate a Marmite reaction, there can be no doubt that his government has been pragmatic in recognising that the globalisation trend that China exploited for 20 years is played out, and that India’s way forwards requires focus upon the creation of a powerful internal national market and structure. The digitalisation of banking, the ID system, the tax office and the welfare schemes are driving to extinction the regional markets, local levy charges and informal cash-based business that just five years ago represented two-fifths of output and 87% of jobs. The national highways are now 50% longer than in 2014. Air freight volumes are up 44%. Air passenger traffic has doubled. The number of mobile-phone base-stations has trebled. As multinationals diversify away from China, Modi’s government has made available $26 billion of subsidies for investment in 14 industries – seeing companies like Samsung now making mobile phones in India. There is still much to be delivered upon – not least growth in corporate investment (India only counts for 2% of the global exports of goods) so that Gopal’s “factory of the world” vision becomes a reality. In this regard, there are clear signs that the firms at the very top of the pyramid – such as Tata, Reliance and JSW are beginning to make very heavy investments in infrastructure and emerging technologies. The three biggest headwinds are firstly, the national infrastructure – characterised by the state owned electricity distributors – bankrupt and unable to deliver consistent supply; secondly, education – still a heinously high number of children not in school; thirdly, and most importantly of all – diversity, inclusion and equality. It is former governor of the Reserve Bank of India, Duvvuri Subbarao who puts it best:

“If we do not take care of inequality, we cant get very far with growth”

This latter point will prove particularly significant in an environment where the attitudes and actions investors and corporates are increasingly driven by ESG focus. A century ago, Mahatma Gandhi saw the simple spinning wheel as the unifier of the nation and the re-generator of its economy. This year, India is in the Chair of the G-20 and whilst today’s emblems of growth are unicorn companies, technology parks and a flashy consumer culture – the underlying requirements are unchanged. There are clear signs that the country is unifying – around growth, and that the government is delivering on promises to roll away the red tape, corruption and the inconsistency of policy that have served as powerful handbrakes for so long. Our club is dedicated to long-term thematic investing and we will remain very focussed on all that India has to offer.

Launched in 2021, Noetic Fund I has returned 400% to date.

Noetic Fund II is raising capital, currently at $40mn.

Sector offers a preferable risk-reward profile today.

Private industry is working hard to alleviate the mental health epidemic.

PTSD, suicide and depression are all growing global concerns.

Expaned focus from psychedelics to mental health solutions.

Why Do You Care?

Noetic’s team understand the psychedelic and mental health space as well as anyone.

The first fund is up 400% and the company is now raising for a second fund when the risks are lower and the return potential is greater.

Regulatory walls are being broken down across multiple nations as governments look to address a global mental health epidemic that is short of solutions and stuck in a repeat prescription mindset that, for too long, has looked to treat symptom rather than cause.

Valuations across the sector have come off dramatically since some major 2021 IPOs, offering an investable universe with a seemingly more favourable risk-reward profile.

CALL SUMMARY

The Epidemic