Our thanks to Director of IR Mark Root for taking the time to explain why NovoNordisk, despite annualising 31% over the past five years and boasting a $350bn market cap, is still considered a growth stock that members may wish to back on account of its low-volatility and exciting new product, Wegovy which the FDA approved for weight management in June 2021.

Similar to its sister drug Ozempic (they share the same molecule semaglutide), which the FDA approved in 2017 to help control blood sugar in type-2 diabetes, Wegovy works by mimicking the action of a naturally occurring hormone glucagon-like peptide 1 or GLP-1 that delays the digestion process & thereby manages appetite.

While only Wegovy is approved for weight management & is prescribed in a higher dosage, Mark noted that Ozempic is also being prescribed off-label & that ~0.5m are currently receiving the 1x week injectable for weight management.

Incredibly, for a mega-cap biopharma stock, Novo Nordisk now guides for 2023 top-line growth of 24%-30% & EBIT growth of 28-34%, with sell-side analysts describing it as a ‘premium growth’ company. It’s a 100-year-old company this year, and at the rate it’s going, who’s to say it won’t be around for another 100?

Bull Points

Current prescriptions for weight management (Wegovy & off-label Ozempic) are ~500k.

The TAM is ~650m worldwide.

Novo produces 40% of the world’s insulin.

Novo has a 32% share of the global diabetes market by value.

Exhibiting high growth and low volatility.

Sell-side analysts see the market for weight management drugs rising to $30-50bn by 2030 (2022 $4bn).

A Ph3 trial for an oral Wegovy could be approved & available by 2024-25

Bear Points

Concentrated portfolio (diabetes 80% group sales).

Eli Lily is expected to receive approval for its GLP-1 weight management drug by YE & launch in 2024.

Prescription drugs only, not available over the counter, reducing TAM.

During the trial, some rodents developed thyroid cancer.

Five-year share price annualised 31% vs EPS growth of 12%.

Diabetes / Ozempic

Historically the company was stagnating, and the share price reflected it. Mark explained that on investor calls ten years back, the company projected single-digit growth, but then everything changed on the back of GLP-1’s & discovery of the molecule semaglutide

Despite its discovery some decades ago, the molecule wasn’t fully utilised for treatment until more recently and enabled Novo Nordisk to introduce new Drugs with its 2017 release of Ozempic for Type II diabetes.

Obesity / Wegovy

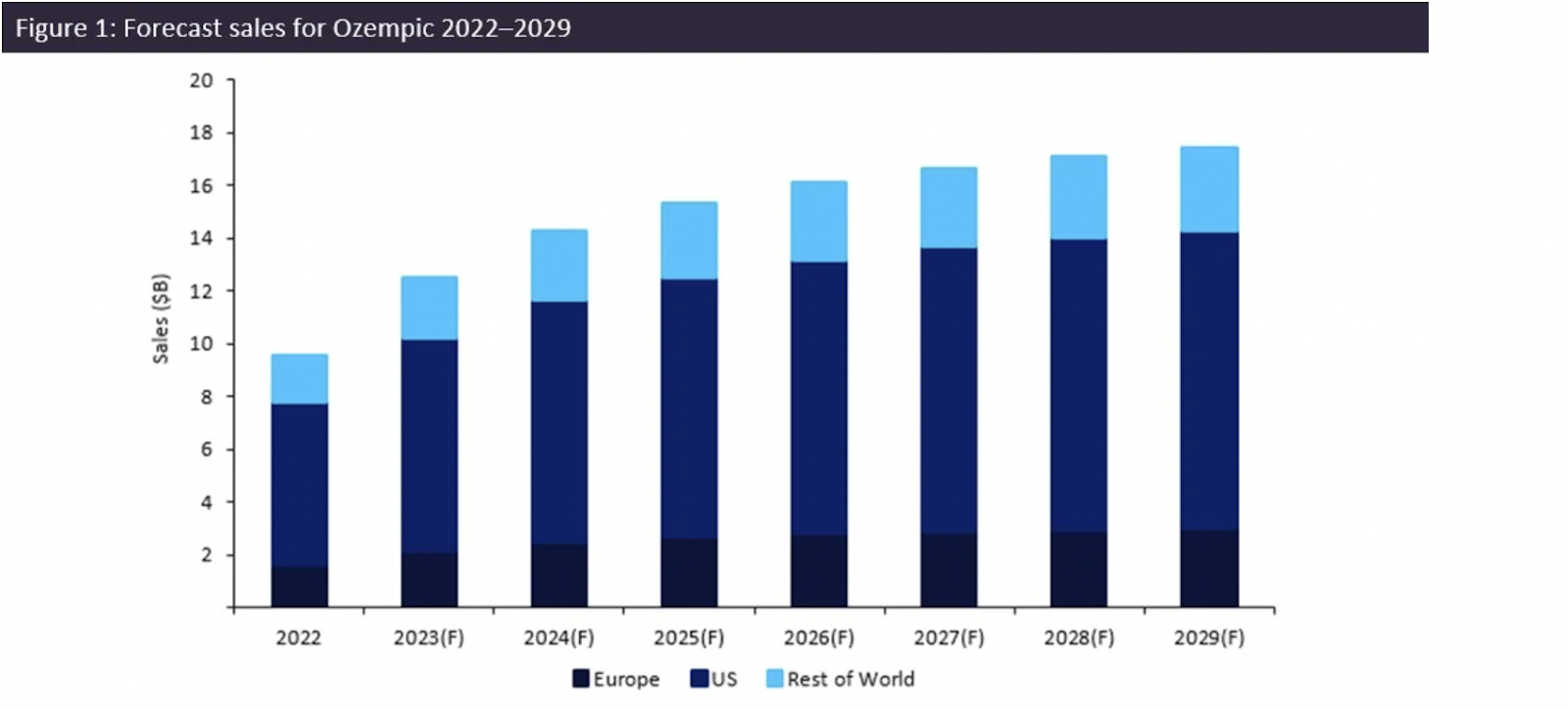

As you can see from the graph above, despite explosive growth since its release, the sales of Ozempic will soon begin to plateau, so the question is, where does the company go now? The share price returns have been extraordinary, and shareholders have been paid handsomely through dividends.

The short answer is Mark believes the P/E multiple of the stock (around 35x) is entirely justified due to the growth potential of the company’s new Wegovy drug. (Pretty sure Mark would not want to be seen to justify or endorse the share price & / or rating)

Like Ozempic, Wegovy is a clinical drug only to be taken under the prescription of a clinician who has ascertained the patient to employ the correct characteristics. Remarkably, it has been shown that the drug resulted in a 17%-18% weight loss over a 68-week period. According to Mark, “Obesity is a burgeoning market, and at Novo Nordisk, we see it as a chronic disease.”

Last year the company sold $0.5n worth of obesity products. But this is a growth market, and the company only treated 500k of a 650mn addressable worldwide market, so the 20-30% sales growth forecast might be doable.

Following our recent Healthcare event, some of our members expressed an interest in learning more about Juvenescence Ltd and their ongoing $150mn capital raise.

For details of our contractual arrangement please see below.*

Executive Summary We recently spoke to Dr. Richard Marshall, CEO of Juvenescence, along with co-founder Dr. Greg Bailey and CFO David Gill who between them presented the case for the company’s outlook, pipeline of biopharma programs that focus on age-related diseases and the forthcoming private placement.

A flurry of capital and institutional interest has moved into the longevity space over the last year or so and the team at Juvenescence believe they are well placed to leave their stamp on the sector. With a diverse portfolio of prospective solutions aimed at clinical diseases, their simple goal is to elongate society’s “healthspan” – that is the duration of your life for which you feel healthy.

Given the perceived velocity at which he believes this sector will boom, according to co-founder Greg Bailey, “this is like if you’d been offered[an investment in] ChatGPT three years ago. Something that’s going to be explosive!”

For supplementary reading, please see this corporate two-pager and the latest investment deck.

The on-demand call recording is available on the website.

Bull Points

A diverse pipeline of 10 products.

One drug (targeting liver disease) which is already through to Phase II testing.

Two products aimed for release in the next 18 months.

Unlike many biopharma investments, a less binary outcome due to product diversification.

A vast addressable market.

$800mn IPO planned for the end of 2024.

Series C investors will receive 25% downside protection.

Down-round, pre-money is $445mn vs Series B investors in at $500mn.

A highly experienced management team.

Co-founder, Jim Mellon, is a member of the Curation Collective investment club.

Bear Points

There’s a risk that the entire portfolio doesn’t reach commercialisation.

It’s a difficult company to put a fair valuation on.

There’s a lot of hype around the space currently.

Pipeline For an overview of the pipeline of products as it stands, we’d recommend reviewing the company’s website or reading the latest deck.

To summarise it though, all of these products aim to address clinical diseases that between them result in the vast majority of human deaths. By tackling these diseases head-on, the company believes they will elongate the healthspan of society.

In addition, one of the company’s strategies is to supplement the portfolio with a collection of supplements due to the lower barrier to entry to market. These are available to buy on the website and include a Metabolic Switch® powder which claims to elevate blood ketones over a long period of time.

Team The following excerpt summaries are largely taken from the website where more information on the management team can be found.

Dr. Richard Marshall, CBE, MD, PhD/ Chief Executive Officer Richard is a physician scientist and a highly experienced executive with a 20-year track record of outstanding leadership in Pharmaceutical R&D.

Dr. Greg Bailey, MD / Executive Chairman and Co-Founder Co-founder and the Executive Chairman of Juvenescence, Greg is a physician, financier, and biotech entrepreneur.

Jim Mellon / Deputy Chairman and Co-Founder Curation Collective club member, Deputy Chairman, co-founder and co-author of Juvenescene: Investing In The Age of Longevity, Jim was inspired by the possibilities and advances being made in the area of longevity.

Dr. Declan Doogan, MD / Board Member and Co-Founder Another co-founder, Declan was driven to start the company because he believes we all can do better in managing health as we get older.

Private Placement With a pre-money valuation of $445mn, the company’s Series C round is looking to raise $150mn ($100k minimum buy-in) in what is anticipated to be its last pre-IPO round.

Juvenescence has programmes with the potential for 3-5 clinical trial starts in the next 18 months. Supported by the Series C proceeds, it is on the cusp of unlocking meaningful value from the pipeline.

Juvenescence’s past fundraise rounds have cumulatively raised $246m since it was established in 2017.

Q&A

Do you plan to bring these drugs to market yourselves?

Juvenescence has the capability to take all drugs through clinical development itself, but many potential partnerships are in the pipeline, including potentially with the likes of Pfizer and Harvard.

In your experience, what percentage of biotech drugs reach Phase I of clinical development and what percentage go on to reach Phase II and eventually come to market?

Around 25-30% of drugs fail at Phase I and at Phase II you can expect to lose an additional 20%. By Phase III, a total of 50% of drugs are lost, so there is a 20-50% of having a succesful Phase II drug.

Given the fact that our portfolio has 10 drugs in the portfolio, we are confident, given the balance of probabilities, that a number of them will come to market.

What’s the difference between your company and a normal biotech company? Will AI be involved in your company?

AI helps with the initial data stage of drug development, finding the right drug target and designing molecules.

As more companies adopt AI, drug development will become much faster and cheaper. Juvencesence has helped spawn an AI drug development company and all products in the current pipeline will benefit from AI in the development process.

Summary

One of the club’s core aims is to invest in areas that are “doing well by doing good.” It’s hard to think of an investment closer to the heart of this concept than one which aims to increase the healthspan of the population by pushing back, and one day maybe even reversing, the aging process.

It’s very difficult to ascertain how much of Juvenescence’s portfolio may be revolutionary and how much of it is well framed around the inherent interest of longevity, and to be honest, only time will tell. What we do know is that valuing this company is no easy task. But the potential addressable market of each product, the downside protection of the placement and the diverse portfolio are all positive.

As with all investments, members are expected to perform their own due diligence, but should you want to know more about the company or the placement, please reach out to james.gourlay@curationcollective.org or reply to this email.

—–

* As mentioned above, following our recent Healthcare event, some of our members expressed an interest in learning more about Juvenescence and their current $150mn capital raise. In response to that interest, we have contracted with the company to act in the capacity of Introductory Agent – and will be holding a call on June 1st at 16:30 BST at which the Juvenescence management will present.

It is always important to stress whenever we act as an introductory agent for a corporate client, we classify you, the members who attend the call and/or take part in the proposed transaction as “corporate finance contacts” as defined by the FCA. This means that in relation to the fundraise, we are not acting on behalf of our members (we are acting on behalf of Juvenescence), and will not be responsible to you for providing protections in relation to the transaction, or be, in any way, advising you. This is the standard position for any financial promotion we take part in on behalf of a corporate client within the FSA regimen in the role of introducing agent to our HNW and/or Sophisticated investors.

We had a fascinating meeting with Axon on Wednesday, the manufacturer of the taser.

Axon tasers and body cameras link to a cloud based software solution called evidence.com that helps police forces analyse stored video footage and fight crime. Axon operates a SaaS model renting the equipment and analytics suite on a monthly basis.

Once a law enforcement agency engages with Axon the company has an almost perfect retention rate which may go some of the way to explaining why the shares have rallied in excess of 400% in the last 5 years. If you believe in increased civil unrest and that incapacitating people is better than killing them, then Axon may be the stock for you!

The valuation does not look cheap on many traditional metrics; but the company believes the total addressable market is $50bn and they currently have revenues of $1.2bn, so plenty to go for over the long term and little in the way of competition. Also look out in future for drones with tasers attached that will hunt criminals down like a wild animal trying to escape a tranquilizer dart from a helicopter. It’s going to be a lot cheaper and safer than putting a chopper in the air, and a big area of growth for the company.